How this social media manager stays cool on $60K a year

Welcome to My Bottom Line, a series where we dive into the net worth, spending, and saving habits of real Canadians.

This month, we chat with a 26-year-old social media manager from Toronto’s West End, who brings in $5,020 a month.

Financial Breakdown

Tell us a bit about yourself

I currently live in the west end of Toronto with my boyfriend. I consider my life pretty typical for a 20-something city dweller. I work as a social media manager for an ad agency. It’s a cool job, even though I find it draining sometimes. In my downtime, I spend a lot of time strolling around my neighbourhood, going for coffee, checking out local home goods stores, and dining out. I spend a good chunk of my weekends moonlighting as a suburbanite, as I often visit my parents in the GTA. It’s a change of scenery; they cook, and there’s always food in the fridge. Plus, there’s the added bonus of relaxing in a space slightly bigger than my junior one bedroom.

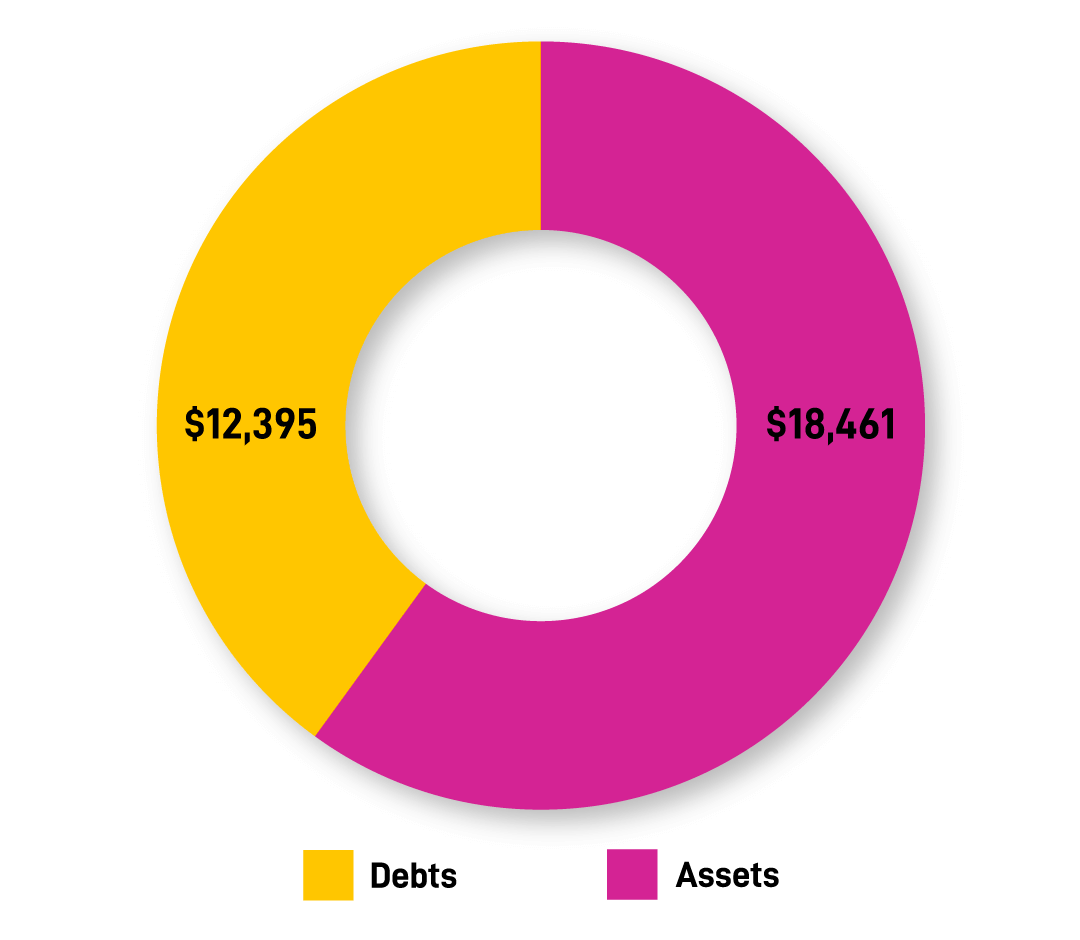

Debt

Student Loans $12,075 – Most of my debt is from student loans. I wasn’t paying them off as quickly as I usually would during the pandemic because I had the advantage of some debt forgiveness, but now I’m back on track trying to pay that down. Since I’ve been a bit more regimented with my budget, I’ve been fortunate to save more than I used to, so I’m hoping to have my student loans completely paid off in the next year or so.

Credit Card $320 – I like to use my cash-back credit card for all my spending and then pay it off as soon as possible. I’ve learned that getting cash back rewards is really worth it with that little adjustment to my spending habits.

Assets

Emergency Fund $3,552.03 – I keep my emergency fund in a Savings Plus Account with EQ Bank. I try to contribute to it every month, and it’s always accumulating compound interest, which is encouraging.

Vacation fund $611.05 – A second EQ Bank Savings Plus Account is where I stash my vacation fund. I’m hoping to go on a trip this fall with my boyfriend, so in the meantime it’s building interest while we wait to book flights.

Investments $14,098 – My investments are in a TFSA with Wealthsimple that I contribute to once a month. I will admit I don’t feel super confident with investing yet, so I use their robo-advisor platform. I’ve lost money this year, but I try not to obsess over it and just trust the process. I’m not sure yet if that money is going towards a house or retirement. It doesn’t feel like enough for either goal right now, but I feel good about how much I’ve been able to build it up at this point.

GIC $200.12 – Earlier this year, I purchased a $200 GIC. It might not sound like a lot, but it’s the beginning of me saving up for something a bit bigger. It’s yet to be determined if it’ll be for a wedding or a car, but my boyfriend and I are working towards one of those two “adulting” purchases – we just don’t know which step is more responsible to take at this point. And hey, if it ends up being the car, we might end up driving somewhere to elope! Weddings can be so expensive, and seeing how people got creative with micro weddings during the pandemic got us inspired.

What’s your money strategy?

I am getting more comfortable with managing my finances responsibly. For a long time, I was irresponsible with my money. I don’t feel super confident with anything more complex than saving and using a cash back credit card. When it comes to investing, I feel like I don’t really know what I’m doing, so I’ve taken advice from friends my age who have a bit more experience in that area.

I have debt, and I want to save, but because my debt interest was at 0% for a long time, I didn’t really feel an urgency to pay it off. In hindsight, I feel like that was the wrong decision. I’m often inclined to just spend my entire paycheque, but I’ve gotten a lot more responsible, especially since being at home during the pandemic gave me a bit of a boost to be able to save more than I was spending.

Did you negotiate your salary? Tell us about how that went.

I did negotiate my salary, yes. Up until about a year ago, I was getting paid about $43K a year, and I discovered I was being very underpaid for my role when I received an offer from another company that was willing to pay me a lot more. I ended up negotiating my salary with my current company, because I’m really happy there. I could be getting paid more, but I feel like my job allows me certain lifestyle benefits such as work life balance. I don’t work 70 hours a week like some of my friends do. I’m happy with my salary now and I think I’m being paid more fairly than I was.

The negotiation was very difficult emotionally for me, and I was really nervous about it. In the end though, I realized it really wasn’t a big deal for my company. My HR department and direct manager were not really surprised when the conversation happened. (I guess they knew they were underpaying me.) I really don’t feel like I’m getting treated any differently now, which in hindsight was my biggest concern. The moral of the story here is to have the conversation. You could be leaving a lot of money on the table otherwise.

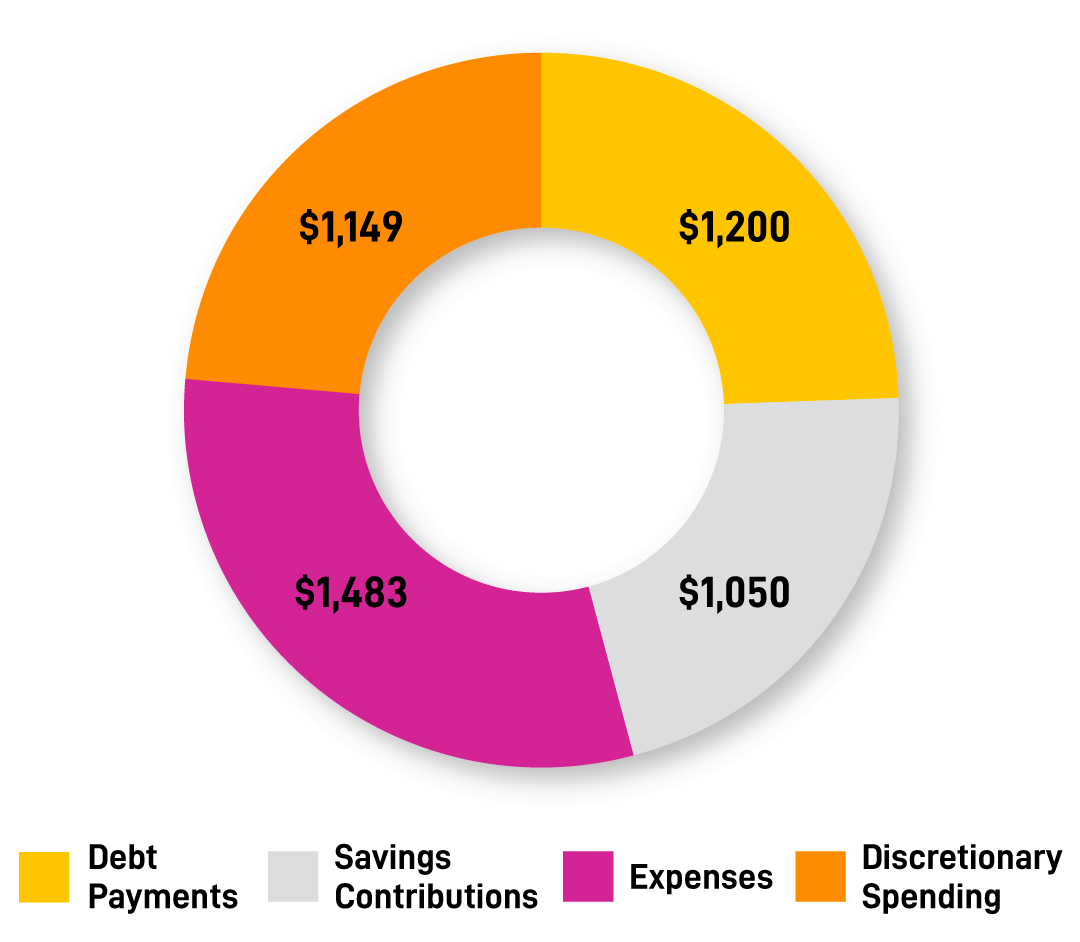

Salary & Monthly expenses

Monthly income (after tax) $4,895

Side hustle $125

Debt payments $1,200

Savings contributions $1,050

Rent $850 – I feel like my rent is pretty reasonable by Toronto standards, and my boyfriend and I split it pretty evenly down the middle.

Transportation $178 – I put about $120 per month on my Presto pass, which I use more often now, because I take the TTC to work and the GO bus to visit my parents. Now that the world has opened up and I’m going out more, I’ll spend money on the occasional Uber, whether that’s coming home late at night, or early in the morning if I’m running late for work.

Cellphone $26 – My cellphone bill looks ridiculously cheap, because work gives me a $60 stipend each month to pay for it. I’m a social media manager, so I use my phone a lot for work, and that tends to include high data charges.

Hydro $76

Internet $80 – Since my salary is higher right now than my boyfriend, I cover our internet and hydro. We needed to upgrade our internet recently to a more robust plan since we both work from home the majority of the time.

Laundry $25

Entertainment $46.50 – Between Netflix, Spotify, Crave, and magazine subscriptions, I spend about $50 a month. I have mostly family plans and I cover the cost for myself and my family.

Groceries $245 – Groceries have been more expensive lately than they used to be – thanks, inflation! We shop at our local budget grocery store pretty often, but you know how it is, you end up needed that one missing ingredient or want to splurge on healthy snacks and all of a sudden, the bill shoots up. We are working on being more responsible with our grocery bill keeping that in mind.

Everyday items $286

Nonessential spending & gifts $556 – This category is a bit high this month. My apartment doesn’t have central air, so I dipped into my savings this month to buy a secondhand AC unit from Facebook marketplace during a major heat wave. It was worth every penny. I also had to get a new dress to wear to a wedding this summer. It ended up being more than I budgeted for, but it seems like another expense that has been really impacted by inflation. I shelled out $150 for the wedding gift, and $50 for a gift card for Father’s Day.

Leisure $260 – This is one area where my boyfriend and I tend to splurge. We’re fortunate to have reasonable rent, so we feel comfortable dining out or grabbing coffee from our local shop. Our favourite date night is going to the movies. My mom buys movie passes from Costco and we pay her back, so we do movie nights quite frequently.

Bank account fees $3.95 – I keep my chequing account because of the one and only thing I still use my debit card for – laundry. Every month I go to the bank to grab actual coins for the washer and dryer in my building.

What are your future plans for housing – do you intend to rent long-term or are you aiming for home ownership?

Right now, a house feels like a completely unattainable goal. This isn’t news to anyone living in Toronto. So my savings account is earmarked for a house or retirement. Now that I live with a partner, a mortgage does feel a bit more attainable than it used to. Prior to that, I felt like home ownership was never going to be financially feasible, which is a big reason why I never really saved for it. Now that we’re a dual income home, we’re thinking about buying a condo eventually if it fits our lifestyle. We’ll reassess once we have close to enough for a down payment (which reasonably won’t be for another 6 years).

What is the worst money advice you’ve ever been given?

I guarantee you haven’t heard this one yet! A family member advised me to do what he did to buy a home – beg, borrow, and steal for a down payment. (Ok, maybe not steal.) When he bought his first home, to amass his down payment, he got loans from family, friends, his boss, and the people who were selling his house. His secondary advice, (and I’m still not always sure if he was serious or kidding) was to “try not to pay them back”. I mean, it worked for him, but his down payment was also $15K … times have changed.

What do you wish you’d been taught about money earlier in life?

I wish I had understood compound interest earlier in life. I had always been told to save my money, but it never felt urgent enough to do it. Of course, now, I wish that I had. But the concept of compound interest was never properly explained to me until I graduated university and I owed interest. Thankfully, at the same time, it was explained to me that compound interest can also work in a positive way. I’ve been working since I was 14, but I didn’t really start to save until my 20s. That’s a lot of interest I could have been earning. It’s hard to think about!

What did you learn about your spending habits from this exercise?

I learned I live a pretty fortunate life, and I should be paying my debt down faster because I do have a good amount of disposable income. I spend way more money on groceries than I thought. It feels like small amounts here and there, but it adds up way more than I thought it was going to, and it’s costing me more than it should.

How is EQ Bank helping you reach your money goals?

Getting my paycheque deposited directly into my EQ Bank Account has really reframed the way I see my money; it means I save first, because I see those funds as savings rather than disposable income. Then I use a cash back credit card for all my spending (and immediately pay it off, usually).

This means the money left over at the end of the month automatically becomes savings, and I don’t have to think about it. In addition, it’s made my chequing account all but obsolete (with the exception of those pesky laundry funds). It’s

really encouraged me to think about saving first. And it makes me think twice when I want to buy something frivolous!

Ready to add more savings to your bottom line? Click here to get started.

Certain identifying details of individuals may have been changed to protect their privacy.