How a 32-year-old living in Calgary travels the world with no credit card debt

Welcome to My Bottom Line, a series where we dive into the net worth, spending, and saving habits of real Canadians.

This month, we chat with a 32-year-old UX designer from Calgary, who brings in $3,870 a month.

Financial Breakdown

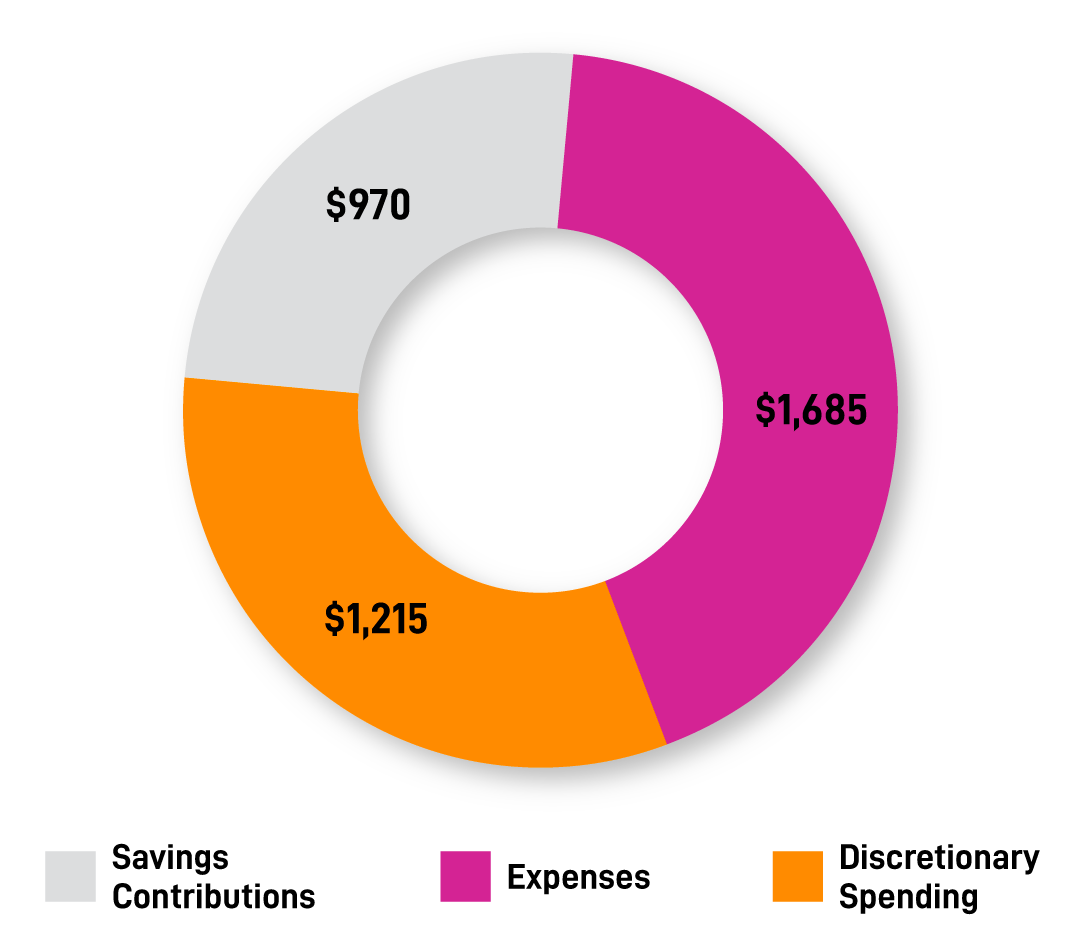

Monthly income after tax - $3,870

Tell us a bit about yourself

I’m pretty introverted, and I work from home, so I spend a fair bit of time there. Typically, I work during the day, and in the evening I read, watch TV, and take my dog for walks in the park. My girlfriend and I don’t live together, so we like to go on date nights, usually out to dinner. We both love food and trying different sweet treats like donuts and specialty ice cream.

I don’t spend a lot of time or money on entertainment. I know that might sound super boring, but that’s the truth!

Debt

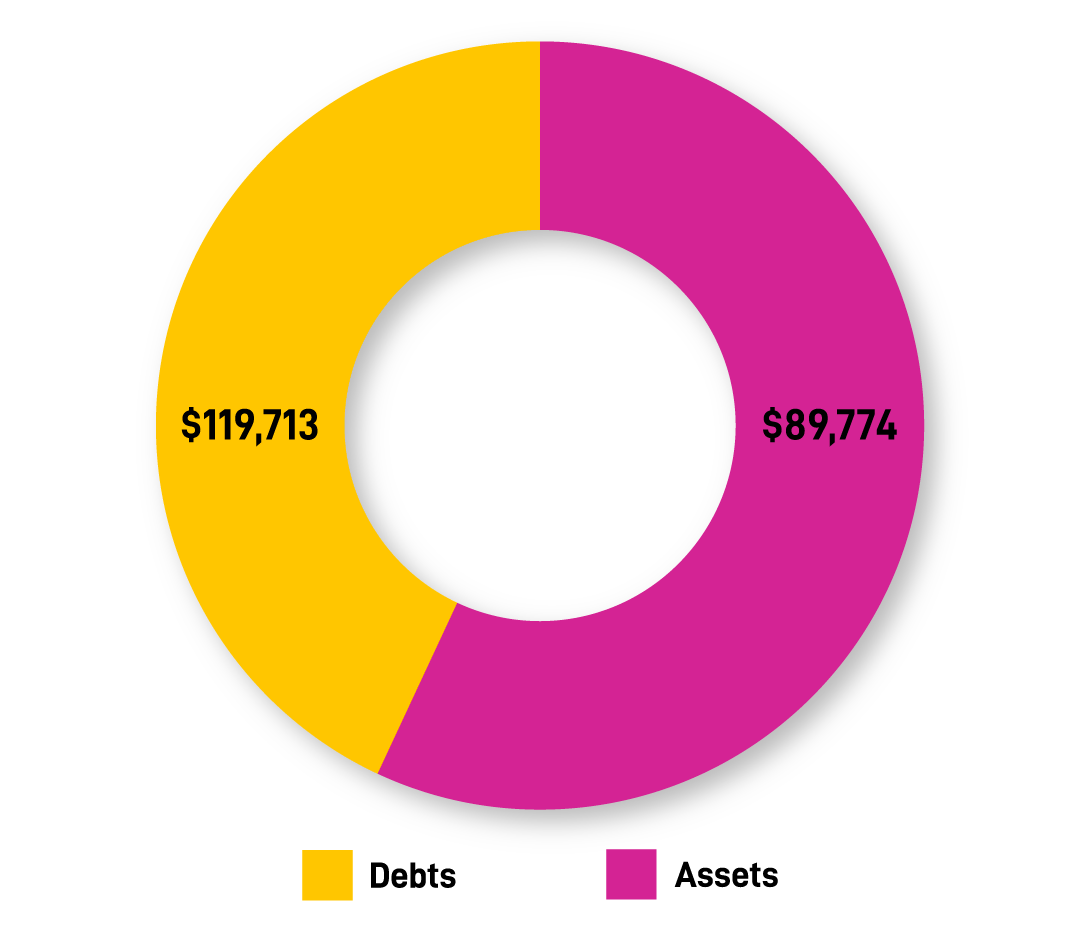

Mortgage - $119,713

My mortgage is my only debt. I have an agreement with myself that I will not carry a balance on my credit card. With that said, I use it for absolutely everything; if I go out for dinner, if I buy clothes, whatever I spend money on, I use my credit card. But that comes with the knowledge that I’m going to pay off the balance in full, so I don’t spend what I can’t afford. With every single paycheque I get, I look up the current balance of my credit card and pay it in full. I get paid bi-weekly, so I’m fully paying off my credit card balance every two weeks.

On the rare occasion where there’s an abnormal expense and I do have to carry a balance, I’ll transfer funds from my line of credit to my credit card to pay it off in full so that I’m carrying a balance with a lower interest rate. Then, I’ll slowly pay that down versus carrying any credit card debt. Credit card interest rates are so high and compound interest adds up so fast that once you get into it, it can be difficult to get out, so I’d rather just avoid it altogether. I’m glad I put in the time to learn about different banking products and understand different financial strategies so I can keep my finances running like a well-oiled machine.

Assets

Tax-Free Savings Account (TFSA) - $77,441

Retirement Savings Plan (RSP) - $11,849

Cryptocurrency - $484

My plans for the future include early retirement. To make this happen, I’m really just trying to save and invest as much as possible. I want to create as many passive income streams for myself as I can, so I don’t have to worry about working longer than I need to.

I have a very small amount of cryptocurrency. A huge strategy I’ve always used in personal finance, is that I learn by doing. It’s almost like an experimentation process. I’ll read, watch YouTube videos, and find out what other people are doing. Then, I’ll formulate a plan of what I think is best for me and try it out. Cryptocurrency isn’t something I’m too knowledgeable about, and to me, it seems like a high-risk investment, so it’s not something I’m gonna go all in on. However, it does pique my curiosity and I want to test the waters.

I invested a very small amount of money in crypto, and I’m learning as I go how to manage it and learning different crypto trading strategies to guide my decision making. When I’m learning like this, it’s important to me to keep the dollar amount low so I’m not losing a ton of money when I don’t know what I’m doing yet. I intentionally invested an amount that I’m willing to lose completely, and it’s a good thing I did, because I ended up losing a lot in the crypto crash this spring. The bottom line when it comes to crypto, my strategy is not to use it to meet my financial goals, it’s a learning experience.

What’s your money strategy?

I’m clearly a very aggressive saver - I probably save more than the typical person. I like to sort of gamify my finances; my strategy is to spend well below my means, so I can save as much as physically possible. My finances are one area of my life where I feel very confident. I’ve spent so much of my time trying to learn as much as I can by reading books, watching videos and listening to podcasts. I didn’t learn anything valuable about personal finance in school, and I didn’t learn a ton about it from my family so this is really something I dug into on my own. I became very passionate about it, and over the years of learning different strategies and trying different things to save and invest, I’m at the point where I can really see tangible results. This gives me the confidence to know that I know what I’m doing. It shows me I’m on the right track.

Did you negotiate your salary? Tell us about how that went.

I have never negotiated my salary. I don’t know how to do it, and I don’t feel very confident in that at all. I came from a really humble background, and I’ll be honest, I make more now than I ever thought I would in life. Negotiating my salary higher, I don’t feel the need to do it. It might be naïve or self-conscious, or maybe I don’t know my own worth, who knows?

I’m not someone who bases my self-worth on my career. I have a decent job, a decent income, and I’m proud of where I’ve gotten myself to. My goal is to get the income I need to invest and save so I can have the future I want. I like to see my paycheques actively building my savings and investments.

Monthly Expenses

Mortgage payments - $568

Property taxes - $82

Condo fees - $375

Electricity - $76

Bus fare - $112

Cellphone - $70

Internet - $65

Groceries - $264

Pet expenses (food/vet) - $73

Savings contributions - $970

Previously, one of my major expenses was my car. I recently moved from the suburbs to the inner city, and a big reason for that was so that I could sell my car. Between car payments, gas, insurance and general upkeep, it was almost as much as my housing, and I didn’t even really drive that much. I could afford it, but it wasn’t really conducive to my strategy of keeping expenses low.

What are your future plans for housing?

I would like to own at least one investment property. My girlfriend and I are discussing buying a property together in the near future, at which point I’ll turn my current condo into a rental property. To get myself there, I’m going to continue to keep my expenses low in order to save as much as possible. I already have enough savings for a down payment for another property, so I’m financially ready for that.

When it comes to real estate investing, there are a number of things that I’d like to try. One of which is making a profit through appreciation, which is something I achieved when I sold my last condo. I’d like to try flipping a property once to see how it works, but it’s something I want to dig a little deeper into to learn a lot more about. I wouldn’t expect to make a huge profit my first time flipping a house, it would be more to experience it firsthand and learn more about it by doing it.

What is the worst money advice you’ve ever been given?

I could go on and on about this! A lot of people from older generations tend to give very outdated financial advice that was sound advice in their time, but isn’t really applicable anymore. For example, one of the main pieces of financial advice they give is to buy a house and never pay rent. They live and breathe by that. In reality, when those people were in their 20s, there were different home values, a different economy, and a whole different working world. In that world, you graduate high school, get married at 20 and buy a house. It’s not like that anymore. So I’d say that particular piece of advice is not entirely accurate for our generation. It’s not comparing apples to apples. Not at all.

We need to acknowledge the realities that buying is not always better than renting. Now, I’m obviously pro home ownership. I love real estate, and I have a mortgage, but there are situations in life when renting can be more beneficial than owning. It can depend on your city, your income, and your goals. These things all factor into the rent versus buy decision. It’s not a one-size-fits-all scenario.

What do you wish you’d been taught about money earlier in life?

Everything! We didn’t really learn any of this in school at all and my family didn’t have a lot of money. I’d consider us lower middle-class. Generally speaking, the attitude surrounding money in my household growing up was that money is hard to come by and should not be spent frivolously. I was almost made to feel guilty by my parents if I wanted something nice for myself. Even something as simple as ordering pizza, my mom might have guilt tripped us because it wasn’t something she could have afforded to do at our age.

What I wish I had learned earlier would be actual financial management strategies, either from my parents or from the school system. I wasn’t taught about banking products, or compound interest, so I took it upon myself to learn. One of the first big breakthroughs I had (like a lot of millennials) was reading The Wealthy Barber when I was in high school. After that, I put in the effort to seek out more information, but it was never presented to me.

Discretionary Spending

Spotify (shared account) - $11

Non-essential shopping - $54

Dining out - $266

Travel - $795

Lottery tickets - $40

Coursera Plus account - $49

What did you learn about your spending habits from this exercise?

I’m so passionate about personal finance, you’d think I would be a very budget-oriented person, but I don’t do a line-by-line budget. Ironically, I don’t know what I spend on food, clothing, or whatever. I tend to clump all of my “spending” together in one big bill. I categorize my money as “commitments” which are my fixed expenses, “savings”, and then everything else is just “spending”.

My approach to my personal finance is very simple – spend as little as possible to save as much as possible. That type of gamification works for me. I say this a lot - it’s called personal finance because it’s personal. You have to find a strategy that works for you.

Growing up, I used to get made fun of for being cheap. Now, it’s one of my biggest points of pride. (Although frugal is the word I would prefer to use.) I’m just smart with my money, y’know? I made my first investment in a GIC at 16 years old, and I’ve experienced a lot of ups and downs over the years. I’ve learned a lot and it’s something I’m really proud of.

I’m clearly a very frugal person, but one thing I am willing to spend on is travel. I want to see the world, so generally when I travel, I don’t have a specific destination in mind. If I stumble across a really good seat sale, that’s where I’ll go. (My girlfriend and I are headed to Fiji this winter from a seat sale!) I love to experience and learn about new cultures and meet new people. In my opinion, travelling is very valuable to expanding my mindset as a human being.

How is EQ Bank helping you reach your money goals?

I get my paycheques direct deposited into my Savings Plus Account. It won’t surprise anyone at this point if I say that I don’t like paying bank fees, so that’s another place I can easily save, while doing my day-to-day banking. Plus, I’m earning interest on anything left over which goes directly into my TFSA at the end of the month. While my money is waiting to be spent, saved or invested, it’s still earning a higher interest rate than I would at most other banks. I really feel like people who don’t use a high-interest savings account are literally leaving money on the table.

Ready to add more savings to your bottom line? Click here to get started.

Certain identifying details of individuals may have been changed to protect their privacy.