Seniors are a diverse group.

We recognize you’re not all affected by the same issues, but certain issues may affect a higher proportion of seniors than those in other age groups That’s why we’ve dedicated this section to information, tips, and resources that may be relevant to this unique demographic.

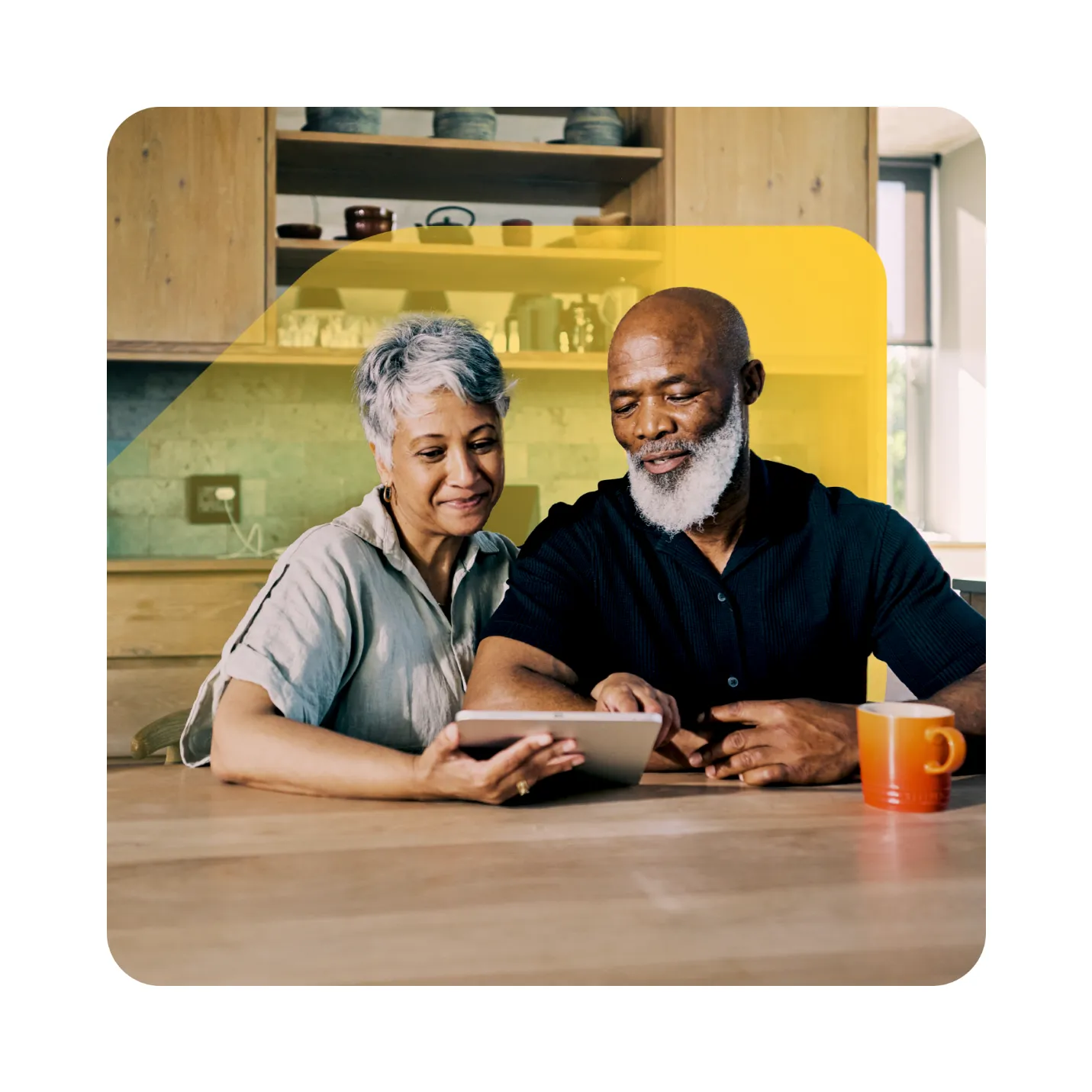

Digital banking: Quick, easy, & totally secure

Banking from the comfort of your home is simple, safe, and secure with EQ Bank.

Your security is important to us. That’s why we make it a priority to provide a secure banking experience anywhere you go. To learn more, read about our EQ Bank Mobile and Online Banking Security Guarantee.

Many day-to-day banking tasks can be done quickly and easily right from your smartphone, tablet, or computer.

Common tasks you can do with EQ Bank—in just a few minutes!

-

Deposit funds

Send money by Interac e-Transfer

-

Pay bills

Deposit cheques using your mobile device

Our Personal Account also comes with a joint account feature.

Power of attorney & joint account: What you need to know

Many Canadians are concerned about how to manage their money, property, and finances as they age or as life changes take place.

It’s a good idea to plan for a time when you may need help, or are unable to deal, with your own finances.

Two tools you can use for managing your financial affairs—and your peace of mind—are:

- power of attorney (POA)

- joint deposit account

A Power of Attorney for Property allows someone to make decisions about your property and finances on your behalf. The terms of the POA outline what an attorney(s) can do on your behalf. For example, they can sign cheques, handle your banking, or even sell real estate for you. It can give you peace of mind that someone you trust will be able to make financial decisions to ensure your well-being in the future.

A joint bank account offers the same features and benefits as a personal chequing or savings account held by one person.

As joint accounts are designed for people who know each other well, make sure you trust who you’re joining up with. Keep in mind, all joint account co-holders have full access to the account and the funds that are in it.

Some other things to think about regarding joint accounts:

- An account co-holder can withdraw all funds from the joint account without your permission

- Account co-holders can view your account transactions

- In the case of a marital breakdown of one of the account co-holders, the account could be considered a matrimonial asset and divided accordingly

Before you use either a POA or joint account, though, it’s important to know how each works, as there are pros and cons to both. The Government of Canada has issued general information, including the advantages, risks, and what to consider for both POAs and joint accounts here.

If you still would like to appoint an attorney after reading the Government of Canada guidance noted above and consulting with your own legal counsel, we would be happy to assist you in this regard by offering you our Power of Attorney Form.

You are under no obligation to use our form. You can provide us with any POA that meets the applicable provincial or territorial requirements and is acceptable to us.

If you choose to use our form, we still encourage you to consult your own legal counsel to discuss it, and how it will impact the management of your financial affairs or other related legal documents you may already have in place.

To learn more about powers of attorney and joint accounts, click here.

Accessibility

At EQ Bank, we’re all about making banking better—for everyone.

As a digital bank, the majority of our banking functions are online. For documents that do require downloading and/or printing, where possible we use a 14-point font size.

While browsing our website, you can make the text larger by using a simple keyboard shortcut:

Keyboard shortcuts on a Mac

Press ⌘ and + (plus) to zoom in

Press ⌘ and - (minus) to zoom out

Press ⌘ and 0 (zero) to return to the default size

Keyboard shortcuts on a PC

Press Ctrl and + (plus) to zoom in

Press Ctrl and - (minus) to zoom out

Press Ctrl and 0 (zero) to return to the default size

Understand elder abuse & financial fraud

Learn how to spot the signs of elder abuse—including financial abuse—and how to protect yourself and others.

Financial abuse is the illegal or unauthorized use of someone else's money or property. It includes pressuring someone for money or property.

To learn more about financial abuse, click here.

Follow these three steps to prevent elder abuse:

-

Protect yourself

What is elder abuse? Stay informed and know your rights to help protect yourself.

-

Learn the signs

Learn the signs and symptoms to find out if you or a senior you know might be experiencing elder abuse or neglect.

-

Reach out

If you think you’re experiencing any form of elder abuse, reach out for help. Here are resources for your province or territory.